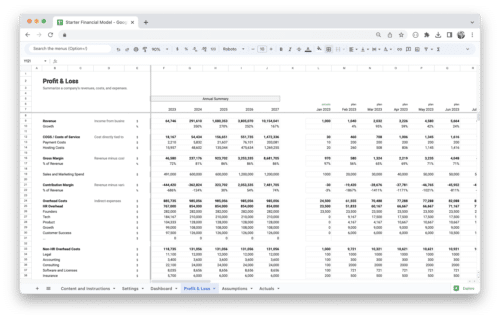

A profit and loss statement is a financial statement that summarizes a business’s revenue, expenses, and net income over a specific period. It provides a snapshot of a business’s financial health and is critical for decision-making, strategic planning, and obtaining financing. This guide will take you through the steps to create a profit and loss statement for your small business.

What is a Profit and Loss Statement?

A profit and loss statement, also known as an income statement, is a financial statement that shows a business’s revenues, expenses, and net income for a specific period. It helps business owners understand their profitability and make informed decisions.

Why is a Profit and Loss Statement Important for Small Business Owners?

A profit and loss statement is crucial for small business owners because it provides an overview of their financial performance. It helps owners identify areas where they can cut costs, increase revenue, and make necessary adjustments to their operations. Additionally, a profit and loss statement is required when applying for loans, seeking investors, or filing taxes.

What Are the Key Components of a Profit and Loss Statement?

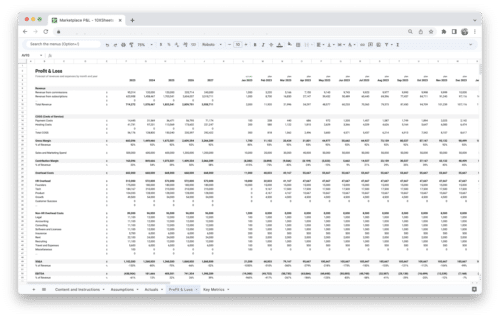

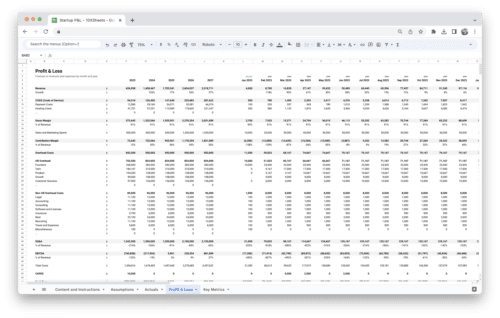

The key components of a profit and loss statement are:

- Revenue: The total money a business earns from sales or services rendered.

- Cost of Goods Sold (COGS): The direct costs of producing goods or services.

- Gross Profit: The difference between revenue and COGS.

- Operating Expenses: The costs of running a business, such as rent, utilities, and salaries.

- Net Income/Loss: The difference between gross profit and operating expenses.

In this guide, we will discuss the steps you need to take to create a profit and loss statement. We will cover everything from gathering financial data to analyzing your statement and making data-driven decisions.

Profit and Loss Statement vs. Balance Sheet

A profit and loss statement and a balance sheet are two different financial statements that serve various purposes. A profit and loss statement shows a business’s revenues, expenses, and net income over a specific period, while a balance sheet shows a business’s assets, liabilities, and equity at a particular point in time.

Who Uses a Profit and Loss Statement?

A profit and loss statement is used by business owners, investors, and lenders to assess a business’s financial health. It helps them understand a business’s profitability and make informed decisions about financing or investing.

Preparing to Create a Profit and Loss Statement

1. Gather Financial Data

The first step in creating a profit and loss statement is to gather your financial data. This includes your income and expenses for the period you’re making the statement for. You can collect this data from your accounting software, bank statements, receipts, and invoices.

2. Choose an Accounting Method

There are two accounting methods that businesses can use: cash basis accounting and accrual accounting. Cash basis accounting records income and expenses when cash is received or paid, while accrual accounting records income and expenses when earned or incurred, regardless of when cash is received or paid.

Most small businesses use cash basis accounting because it is simpler and easier to understand. However, some businesses may benefit from using accrual accounting, especially if they have a lot of inventory or accounts receivable.

3. Determine the Time Period for Your Statement

The next step is determining the period for which you want to create the profit and loss statement. Depending on your business’s needs, this can be a month, quarter, or year.

4. Common Mistakes to Avoid

When creating a profit and loss statement, there are some common mistakes to avoid, such as:

- Not categorizing expenses correctly: Make sure you categorize your expenses correctly so you can accurately analyze your statement.

- Forgetting to include all income: Make sure you include all your income, including any refunds or rebates you may have received.

- Not separating personal and business expenses: Make sure you separate your personal and business expenses so you can accurately track your business’s finances.

How to Make a Profit and Loss Statement?

Now that you have gathered your financial data and determined the reporting duration and accounting method, it’s time to build your profit and loss statement.

1. Revenue

Revenue is the total amount of money a business earns from sales or services rendered. There are two types of revenue:

- Sales revenue: The amount of money a business earns from the sale of goods or services.

- Other revenue: The amount of money a business earns from other sources, such as interest or rent.

To calculate revenue, you can use the following formula:

Total Revenue = Sales Revenue + Other Revenue

2. Cost of Goods Sold (COGS)

The cost of goods sold (COGS) is the direct costs associated with producing goods or services. This includes the cost of raw materials, labor, and manufacturing overhead.

To calculate COGS, you can use the following formula:

3. Gross Profit

Gross profit is the difference between revenue and COGS. It represents the money a business earns after accounting for the costs associated with producing goods or services.

To calculate gross profit, you can use the following formula:

Gross Profit = Total Revenue – COGS

4. Operating Expenses

Operating expenses are the costs associated with running a business, such as rent, utilities, and salaries. These expenses are deducted from gross profit to arrive at net income.

Some common operating expenses include:

- Rent

- Utilities

- Salaries and wages

- Marketing and advertising expenses

- Office supplies

To calculate operating expenses, add up all your expenses for the period you’re creating the statement for.

5. Net Income/Loss

Net income/loss is the difference between gross profit and operating expenses. It represents the money a business earns or loses after accounting for all expenses.

To calculate net income/loss, you can use the following formula:

Net Income/Loss = Gross Profit – Operating Expenses

6. Interpreting the Numbers: Key Performance Indicators

Interpreting your profit and loss statement can be challenging, especially if you’re unfamiliar with accounting terminology. However, by calculating and analyzing key performance indicators (KPIs), you can gain a better understanding of your business’s financial health. Some common KPIs include:

- Gross Margin: The percentage of revenue that is left after deducting COGS.

Gross Margin = (Total Revenue – COGS) / Total Revenue * 100

- Operating Expenses Ratio: The percentage of revenue used to cover operating expenses.

Operating Expenses Ratio = Operating Expenses / Total Revenue * 100

- Net Income Margin: The percentage of revenue left after deducting all expenses, including taxes.

Net Income Margin = Net Income / Total Revenue * 100

Analyzing these KPIs can help you identify areas of your business that need improvement and make data-driven decisions.

How to Analyze a Profit and Loss Statement?

Once you have created your profit and loss statement, it’s time to analyze it.

1. Identifying Areas for Improvement

To identify areas for improvement, you need to analyze your statement and identify areas where you can cut costs, increase revenue, or adjust your operations.

Some ways to analyze your statement include:

- Comparing it to previous periods: This will help you identify any trends or changes in your business’s financial performance.

- Comparing it to industry averages: This will help you identify areas where your business may be underperforming compared to your competitors.

- Benchmarking against KPIs: This will help you identify areas where you can improve your business’s profitability.

2. Making Data-Driven Decisions

After analyzing your statement, you need to make data-driven decisions to improve your business’s financial performance.

Some ways to make data-driven decisions include:

- Adjusting prices: If your gross margin is low, you may need to increase your prices to improve profitability.

- Reducing costs: If your operating expenses ratio is high, you may need to lower your expenses to improve profitability.

- Cutting unnecessary expenses: If you have costs that aren’t contributing to your business’s profitability, you may need to cut them.

3. Preparing for Tax Season

Finally, it’s essential to prepare for tax season by understanding the tax deductions and credits available to small businesses.

Some standard deductions and credits include:

- Business expenses: You can deduct expenses necessary and ordinary for running your business, such as rent, utilities, and office supplies.

- Depreciation: You can deduct the cost of business assets over their useful life.

- Employee benefits: You can deduct the cost of employee benefits, such as health insurance and retirement plans.

- Research and development: You may be eligible for tax credits for conducting research and development activities.

It’s crucial to consult with a tax professional to ensure you’re taking advantage of all the deductions and credits available to your business.

Conclusion

Creating a profit and loss statement is critical for small business owners. It provides an overview of your financial performance and helps you make data-driven decisions to improve profitability. By following the steps outlined, you can create an accurate profit and loss statement and use it to analyze your business’s financial health. Remember to regularly review and update your statement to ensure your business is on track to meet its financial goals.

Get Started With a Prebuilt Template!

Looking to streamline your business financial modeling process with a prebuilt customizable template? Say goodbye to the hassle of building a financial model from scratch and get started right away with one of our premium templates.

- Save time with no need to create a financial model from scratch.

- Reduce errors with prebuilt formulas and calculations.

- Customize to your needs by adding/deleting sections and adjusting formulas.

- Automatically calculate key metrics for valuable insights.

- Make informed decisions about your strategy and goals with a clear picture of your business performance and financial health.